We are about to soft land in about two months

Disregard the immediate speculation surrounding the Federal Reserve's actions this week; we are on course for a smooth economic adjustment within the next two months.

Disregard the immediate speculation surrounding the Federal Reserve's actions this week; we are on course for a smooth economic adjustment within the next two months. The market exhibited a skittish response to the Federal Open Market Committee (FOMC) meeting today, with the Fed maintaining its policy rates as anticipated. However, during the press conference, Jay Powell emphasized that rate reductions would not be considered until there's greater assurance regarding the trajectory of inflation.

The likelihood of rate cuts by the March FOMC meeting dropped to 35% from 50%, though expectations for May remain high at around 100%. Despite this adjustment, market sentiment still predicts six rate cuts throughout the year, a perspective I share.

To clarify, a "soft landing," as defined by the Federal Reserve and echoed by the Britannica dictionary, is akin to a smooth, controlled landing of an aircraft that avoids damage. For an economy, it means the Fed successfully raises interest rates to curb inflation without significantly increasing unemployment or leading to negative GDP growth.

This is precisely what we're witnessing (below chart): a significant policy rate increase of 5.25% since 2022, alongside a decrease in inflation and stable unemployment rates, signaling a successful maneuver.

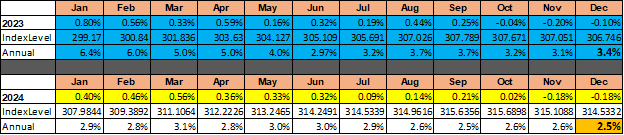

Here is the inflation (CPI) path of 2023 and the row highlighted in yellow projects the inflation’s trajectory for 2024, based on trends observed over the past 23 years since 2000. This projection suggests a promising start to 2024, with a sharp decline in annual inflation potentially leading to the Federal Reserve's first interest rate cut in March. The forecast for the remainder of the year is less certain, with fluctuations expected until the July inflation figures are released. By December's end, annual inflation could reduce to 2.5%, enabling the Federal Reserve to adjust rates six times throughout the year while maintaining positive real rates. In this scenario, the upper bound of Fed target rates ends at 4% leaving real rates around 1.5% which is still restrictive according to Fed’s long-run projections of a 0.5% real rate.

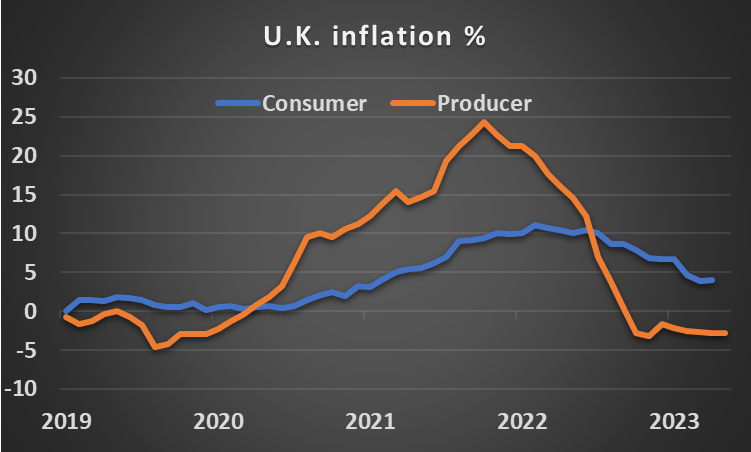

The difficult inflationary months of 2024 will be March, April, May and June but the U.S. is not alone in this game. Deflationary trends are global, and here are the recent inflation figures from major economies. Note that the producer inflation – which usually leads the consumer inflation- is in extreme negative territory for almost all major economies. Notably in China, both consumer and producer inflation are in negative territory.

Germany’s producer inflation hit -8.6% last year.

In the U.K. producer prices are not as bad as in Germany but still down -2.8% last year.

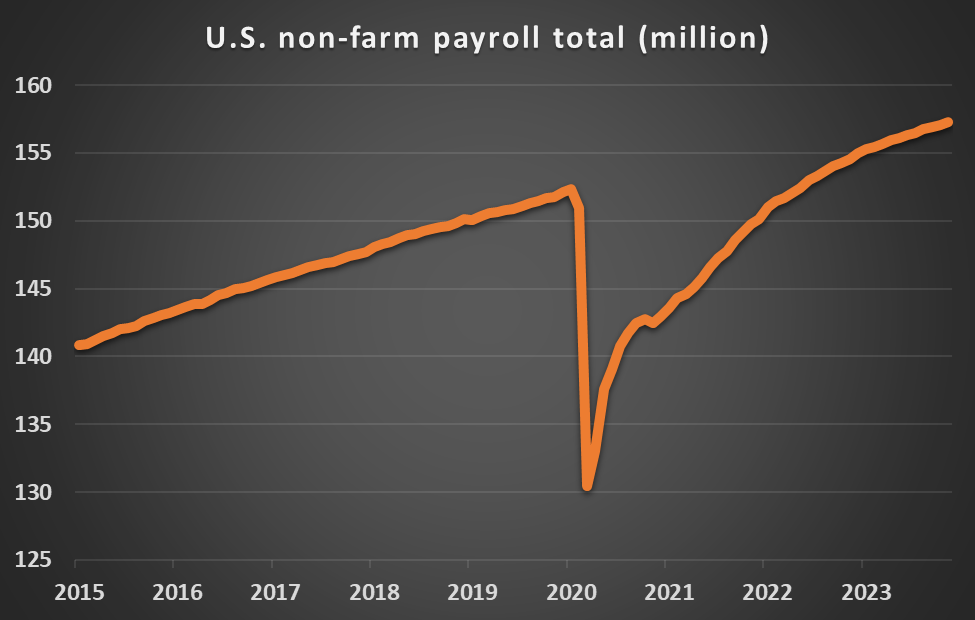

Given global inflation trends and economic slowdowns in China and Europe, I anticipate inflation rates to fall below historical averages in the next three months. For a soft landing, it's crucial that inflation reduction doesn't negatively impact unemployment. U.S. non-farm payroll data shows continued job growth, with 157 million people employed, marking a record high for 19 consecutive months.

In 2023, the U.S. economy added 2.7 million jobs, a 1.8% increase, with real wages up by 0.8%. Given the economy's heavy reliance on consumption, these factors are vital for sustaining economic growth. For 2024, the focus is on job creation and wage growth continuity. With 9 million job openings and 6 million job seekers, a realistic expectation is the creation of 100k new jobs monthly, alongside a 0.4% real wage growth rate semi-annually, leading to a 1.2% GDP growth projection for 2024. The IMF's recent global economic outlook notably upgraded the U.S. among developed economies, projecting a 2.1% economic growth, likely assuming a 200k monthly job increase.

In summary, the U.S. economy maintains a robust position, with ongoing job growth and wage increases that are sustainable rather than destabilizing. Consumers are adjusting or have adjusted to the realities of pricing, modifying their spending habits accordingly, yet overall retail sales are poised to contribute positively to the economy's real growth. Furthermore, inflation is decreasing, both domestically and worldwide. The United Nations' global food and agriculture price index has fallen 25% from its peak, indicating a trend that favors reduced inflation rates in the near future.

Claudia Sahm, a former Fed economist, has articulated potential issues with delaying rate cuts until May. I concur with Sahm's view that immediate rate reductions are advisable, potentially setting a precedent for other central banks, like the ECB, to follow suit. The release of January's inflation data on February 13th is anticipated to be a pivotal moment for global markets.

Here is the link for her blog: